Greetings,

We hope you found our previous post on open-ended, fixed maturity funds, both useful and informative. If you haven’t had a chance to read it yet, we’ve put it here so you don’t miss out!

While 2020 ushered in a global crisis on a scale that humanity had never seen before, 2021 continues to teach us hard lessons earned over decades of practicing unsustainable economics. Pollution, strip-mining, deforestation, over-fishing, and hunting animals to extinction are just a few examples of the effect our economies have on the environment. As the world tries to move forward from the mistakes of the past, one of the things we’re trying to focus on is sustainability, and not taking more from the environment than we can put back. This focus is being delivered right at the root of our financial ecosystem by changing the way responsible investors invest their money.

Measuring sustainability

Sustainability today is measured in terms of E, S, and G, which stands for environmental, social, and governance respectively. Organizations that wish to be ESG compliant need to adhere to a stringent set of standards and regulations. While the environment score is determined by carbon footprint and the impact an organization has on the environment, the social aspect pertains to gender equality, social diversity, racial diversity, as well as diversity based on sexual orientation.

The governance aspect, today, has a lot to do with the ESG data that an organization makes available to the public, the quality of that data, as well as its transparency in operations. This is because financial disclosure and transparency are key aspects of ethical governance and organizations that are in compliance automatically become a much safer choice for investors. Given a choice between full disclosure and ambiguous operations, most investors would choose the former.

Indian ESG Funds

While assets managed by ESG funds globally reached a total of $1.65 trillion as of the December quarter of 2020, assets managed by ESG funds in India reached about 45 billion INR and continue to grow steadily. This is undoubtedly due to the effect the global pandemic has had on people and businesses around the globe. ESG funds weren’t that common pre-pandemic, however, 2020 saw a number of large asset management companies launch ESG schemes in India like the ones listed below.

Aditya Birla Sun Life ESG Fund

1.Started in December 2020 and managed by Mr. Satyabrata Mohanty.

2.Management is active while investments are 60-80% in large cap and remaining in mid and small caps.

3.Portfolio is focused 40-50 ESG compliant companies.

4.The fund retains the right to invest 35% of the fund’s net assets in ESG compliant international securities.

Axis ESG Fund

1.Started in February 2020 and managed by Mr. Jinesh Gopani.

2.This fund is focused on 52 ESG compliant holdings, the top 5 of which include Bajaj Finance, Kotak Mahindra Bank, HDFC Bank, Avenue Supermarts, and Tata Consultancy Services.

3.Management is active and return are at 31.20% since the fund’s inception on December 23, 2020.

4.Investments are 80% in stocks that rate highly on ESG factors.

ICICI Prudential ESG Fund

1.Started on October 2020 and managed by Mr. Mrinal Singh.

2.This fund is focused on 30 ESG compliant holdings, the top 5 of which include HDFC Bank, Kotak Mahindra Bank, Housing Development Finance Corp, Infosys, and Reliance Industries Ltd.

3.Management is active and return are at 10.90% since the fund’s inception on December 23, 2020.

4.Investment are predominantly in companies with a high ESG score. Stock selection is based on internal research as well as the Nifty ESG universe. The fund also reserves the right to invest in international organizations that are ESG compliant.

SBI Magnum Equity ESG Fund

1.Originally named SBI Magnum Equity Fund, this fund was relaunched as SBI Magnum Equity ESG Fund in May 2018 and managed by Mr. Ruchit Mehta.

2.This fund is focused on 39 ESG compliant holdings, the top 5 of which include HDFC Bank, Infosys, Tata Consultancy Services, Reliance Industries Ltd, and ICICI Bank.

3.Management is active and returns are at 10.84% as of December 23, 2020.

4.Investments are 80% in ESG compliant equity, while the remaining 20% in other equities, debt, or money market instruments.

Kotak ESG Opportunities Fund

1.Launched on December 2020 and managed by Mr. Harsha Upadhyaya.

2.This fund is focused on 48 ESG compliant holdings including Infosys,Bharti Airtel, HDFC Bank, Tata Consultancy Services, Eicher Motors,Larsen and Tourbo, Axis Bank, Ultratech Cement, Cipla, and more.

3.Investment is 95% in ESG compliant Indian stocks, 57.84% of which is in large-cap stocks, while 17.95% is in mid-cap stocks, and 9.63% is in small-cap stocks.

In conclusion, the world has changed in terms of environmental awareness and social consciousness and as responsible citizens of the world it is our duty to follow suit. Please feel free to contact us for more information on investing in ESG funds.

Traditionally Indians are bound to the practice of Savings. There is a deep-rooted sense of managing the income by spending less and postponing the luxuries of life. But this ‘saving culture’ has come under threat. The change in mindset is very evident with the youth and the EMI fixated middle-aged salary earners, who are impressed with the easy spending consumer culture of the west.

But the recent global pandemic has exposed the virtues of savings. Even after pay cuts people have realised the power of saving money and planning for the future. Today, those who saved and invested wisely are secure in their lives and livelihood. Their past course of action brings to light the quintessential question running in everyone’s mind “How much to save to plan a secure future”.

The truth be told there is no one size fit all planning strategy for savings. But a general thumb rule to start saving is to start analyzing spending.

1. What is Sovereign Gold Bond (SGB)? Who is the issuer?

SGBs are government securities denominated in grams of gold. They are substitutes for holding physical gold. Investors have to pay the issue price in cash and the bonds will be redeemed in cash on maturity. The Bond is issued by Reserve Bank on behalf of Government of India.

2. Why should I buy SGB rather than physical gold? What are the benefits?

The quantity of gold for which the investor pays is protected, since he receives the ongoing market price at the time of redemption/ premature redemption. The SGB offers a superior alternative to holding gold in physical form. The risks and costs of storage are eliminated. Investors are assured of the market value of gold at the time of maturity and periodical interest. SGB is free from issues like making charges and purity in the case of gold in jewellery form. The bonds are held in the books of the RBI or in demat form eliminating risk of loss of scrip etc.

3. Are there any risks in investing in SGBs?

There may be a risk of capital loss if the market price of gold declines. However, the investor does not lose in terms of the units of gold which he has paid for.

4. Who is eligible to invest in the SGBs?

Persons resident in India as defined under Foreign Exchange Management Act, 1999 are eligible to invest in SGB. Eligible investors include individuals, HUFs, trusts, universities and charitable institutions. Individual investors with subsequent change in residential status from resident to non-resident may continue to hold SGB till early redemption/maturity.

5. Whether joint holding will be allowed?

Yes, joint holding is allowed.

6. Can a Minor invest in SGB?

Yes. The application on behalf of the minor has to be made by his/her guardian.

7. Where can investors get the application form?

The application form will be provided by the issuing banks/SHCIL offices/designated Post Offices/agents. It can also be downloaded from the RBI’s website. Banks may also provide online application facility.

8. What are the Know-Your-Customer (KYC) norms?

Every application must be accompanied by the ‘PAN Number’ issued by the Income Tax Department to the investor(s).

9. Can an investor hold more than one investor ID for subscribing to the Sovereign Gold Bond?

No. An investor can have only one unique investor Id linked to any of the prescribed identification documents. The unique investor ID is to be used for all the subsequent investments in the scheme. For holding securities in dematerialized form, quoting of PAN in the application form is mandatory.

10. What is the minimum and maximum limit for investment?

The Bonds are issued in denominations of one gram of gold and in multiples thereof. Minimum investment in the Bond shall be one gram with a maximum limit of subscription of 4 kg for individuals, 4 kg for Hindu Undivided Family (HUF) and 20 kg for trusts and similar entities notified by the government from time to time per fiscal year (April – March). In case of joint holding, the limit applies to the first applicant. The annual ceiling will include bonds subscribed under different tranches during initial issuance by Government and those purchased from the secondary market. The ceiling on investment will not include the holdings as collateral by banks and other Financial Institutions.

11. Can each member of my family buy 4Kg in their own name?

Yes, each family member can buy the bonds in his/her own name if they satisfy the eligibility criteria as defined at Q No.4.

12. Can an investor/trust buy 4 Kg/20 Kg worth of SGB every year?

Yes. An investor/trust can buy 4 Kg/20 Kg worth of gold every year as the ceiling has been fixed on a fiscal year (April-March) basis.

13. Is the maximum limit of 4 Kg applicable in case of joint holding?

The maximum limit will be applicable to the first applicant in case of a joint holding for that specific application.

14. What is the rate of interest and how will the interest be paid?

The Bonds bear interest at the rate of 2.50 per cent (fixed rate) per annum on the amount of initial investment. Interest will be credited semi-annually to the bank account of the investor and the last interest will be payable on maturity along with the principal.

15. Who are the authorized agencies selling the SGBs?

Bonds are sold through offices or branches of Nationalised Banks, Scheduled Private Banks, Scheduled Foreign Banks, designated Post Offices, Stock Holding Corporation of India Ltd. (SHCIL) and the authorised stock exchanges either directly or through their agents.

16. If I apply, am I assured of allotment?

If the customer meets the eligibility criteria, produces a valid identification document and remits the application money on time, he/she will receive the allotment.

17. When will the customers be issued Holding Certificate?

The customers will be issued Certificate of Holding on the date of issuance of the SGB. Certificate of Holding can be collected from the issuing banks/SHCIL offices/Post Offices/Designated stock exchanges/agents or obtained directly from RBI on email, if email address is provided in the application form.

18. Can I apply online?

Yes. A customer can apply online through the website of the listed scheduled commercial banks. The issue price of the Gold Bonds will be ₹ 50 per gram less than the nominal value to those investors applying online and the payment against the application is made through digital mode.

19. At what price the bonds are sold?

The nominal value of Gold Bonds shall be in Indian Rupees fixed on the basis of simple average of closing price of gold of 999 purity, published by the India Bullion and Jewelers Association Limited, for the last 3 business days of the week preceding the subscription period.

20. Will RBI publish the rate of gold applicable every day?

The price of gold for the relevant tranche will be published on RBI website two days before the issue opens.

21. What will I get on redemption?

On maturity, the Gold Bonds shall be redeemed in Indian Rupees and the redemption price shall be based on simple average of closing price of gold of 999 purity of previous 3 business days from the date of repayment, published by the India Bullion and Jewelers Association Limited.

22. How will I get the redemption amount?

Both interest and redemption proceeds will be credited to the bank account furnished by the customer at the time of buying the bond.

23. What are the procedures involved during redemption?

The investor will be advised one month before maturity regarding the ensuing maturity of the bond.

On the date of maturity, the maturity proceeds will be credited to the bank account as per the details on record.

In case there are changes in any details, such as, account number, email ids, then the investor must intimate the bank/SHCIL/PO promptly.

24. Can I encash the bond anytime I want? Is premature redemption allowed?

Though the tenor of the bond is 8 years, early encashment/redemption of the bond is allowed after fifth year from the date of issue on coupon payment dates. The bond will be tradable on Exchanges, if held in demat form. It can also be transferred to any other eligible investor.

25. What do I have to do if I want to exit my investment?

In case of premature redemption, investors can approach the concerned bank/SHCIL offices/Post Office/agent thirty days before the coupon payment date. Request for premature redemption can only be entertained if the investor approaches the concerned bank/post office at least one day before the coupon payment date. The proceeds will be credited to the customer’s bank account provided at the time of applying for the bond.

26. Can I gift the bonds to a relative or friend on some occasion?

The bond can be gifted/transferable to a relative/friend/anybody who fulfills the eligibility criteria (as mentioned at Q.no. 4). The Bonds shall be transferable in accordance with the provisions of the Government Securities Act 2006 and the Government Securities Regulations 2007 before maturity by execution of an instrument of transfer which is available with the issuing agents.

27. Can I use these securities as collateral for loans?

Yes, these securities are eligible to be used as collateral for loans from banks, financial Institutions and Non-Banking Financial Companies (NBFC). The Loan to Value ratio will be the same as applicable to ordinary gold loan prescribed by RBI from time to time. Granting loan against SGBs would be subject to decision of the bank/financing agency, and cannot be inferred as a matter of right.

28. What are the tax implications on i) interest and ii) capital gain?

Interest on the Bonds will be taxable as per the provisions of the Income-tax Act, 1961 (43 of 1961). The capital gains tax arising on redemption of SGB to an individual has been exempted. The indexation benefits will be provided to long terms capital gains arising to any person on transfer of bond.

29. Is tax deducted at source (TDS) applicable on the bond?

TDS is not applicable on the bond. However, it is the responsibility of the bond holder to comply with the tax laws.

30. Who will provide other customer services to the investors after issuance of the bonds?

The issuing banks/SHCIL offices/Post Offices/Designated stock exchanges/agents through which these securities have been purchased will provide other customer services such as change of address, early redemption, nomination, grievance redressal, transfer applications etc.

31. What are the payment options for investing in the Sovereign Gold Bonds?

Payment can be made through cash (upto ₹ 20000)/cheques/demand draft/electronic fund transfer.

32. Whether nomination facility is available for these investments?

Yes, nomination facility is available as per the provisions of the Government Securities Act 2006 and Government Securities Regulations, 2007. A nomination form is available along with Application form. An individual Non - resident Indian may get the security transferred in his name on account of his being a nominee of a deceased investor provided that:

the Non-Resident investor shall need to hold the security till early redemption or till maturity; and

the interest and maturity proceeds of the investment shall not be repatriable.

33. Can I get the bonds in demat form?

Yes. The bonds can be held in demat account. A specific request for the same must be made in the application form itself.

Till the process of dematerialization is completed, the bonds will be held in RBI’s books. The facility for conversion to demat will also be available subsequent to allotment of the bond.

34. Can I trade these bonds?

The bonds are tradable from a date to be notified by RBI. (It may be noted that only bonds held in de-mat form with depositories can be traded in stock exchanges) The bonds can also be sold and transferred as per provisions of Government Securities Act, 2006. Partial transfer of bonds is also possible.

35. What is the procedure to be followed in the eventuality of death of an investor?

The nominee/nominees to the bond may approach the respective Receiving Office with their claim. The claim of the nominee/nominees will be recognized in terms of the provision of the Government Securities Act, 2006 read with Chapter III of Government Securities Regulation, 2007. In the absence of nomination, claim of the executors or administrators of the deceased holder or claim of the holder of the succession certificate (issued under Part X of Indian Succession Act) may be submitted to the Receiving Offices/Depository. It may be noted that the above provisions are applicable in the case of a deceased minor investor also. The title of the bond in such cases too will pass to the person fulfilling the criteria laid down in Government Securities Act, 2006 and not necessarily to the Natural Guardian.

36. Can I get part repayment of these bonds at the time of exercising put option?

Yes, part holdings can be redeemed in multiples of one gm.

Sources : Reserve Bank of India

The current situation in the world has got a lot of people looking back and wishing they had saved some money for a rainy day because it’s been a pretty rainy year so far. The ability or the inclination towards saving money isn’t really a quality associated with the current generation of “millennials” who could learn a thing or two from generation X in this regard. Now, this isn’t a post about mutual funds, or stocks, or foreign exchange, but rather about the first, most basic, risk-free, baby-step that you can take right now.

If you’ve ever worked a nine to five, you probably already know what a provident fund or PF is. You suffer a little deduction in your salary every month in order to ensure you get a decent chunk of cash when you decide to quit or retire. The public provident fund is similar in the sense that it’s guaranteed by the central government and there’s no way you can lose money on it. The similarities end there, however, as anyone can open a PPF account and you don’t need to be working for an organization.

All you need to do to open a PPF account is walk into bank or post-office with some basic identification and about Rs.500 or you can do it online.The fact that you not only get 7% interest on your money annually, which is more than any fixed deposit or savings account is going to offer you, but also income tax deductions for the amount invested makes this an attractive investment for your portfolio. Additionally, any interest received is exempt from tax, and so is the entire amount on maturity, making the opportunity cost of not having a PPF quite high.

Now saving money takes discipline, especially with schemes with fixed recurring deposits where you incur penalties for failure to pay on time. The reason we call the PPF a “baby-step,” is because even an individual who lacks discipline can see this one through to the end with relative ease. This is because there’s virtually unlimited flexibility in how much you want to invest every year with the minimum being Rs.500 and the maximum Rs.150,000.

While the choice is yours, that’s a really huge range and it can be difficult to set a target and stick to it when you don’t really have to. That being said,flexibility is always a good thing, especially in current times. The only catch, if we have to call it that, is that this is long term investment and maturity is after fifteen years. While there are ways to pay a penalty and cash out after 6 years, the plus side is that even a court can’t order you to settle a debt through your PPF account, so it’s basically safe even if you go bankrupt.

Eligibility: Resident Indians

Returns : Guaranteed

Lock In : 15 Years

Taxation : Tax Benefit under section 80c

Maturity : Tax Free

Minimum Investment :Rs 500/-

Maximum Investment :Rs. 1,50,000/-

In conclusion, getting a PPF account is an essential to your investment portfolio, especially with the higher than average interest rate, risk-free factor, tax benefits, and super-flexible payment options.

While we all have a lot of hopes, dreams, and ambitions growing up, retiring on a quiet beach or in a cozy hill-station is the ultimate happy ending to whatever your life story has been up until now. Unlike in most fairy tales and movies where people grow old and automatically live happily ever after, retirement in real life takes proper planning and a lot of discipline.

Retirement Planning

Keeping in mind the fact that India has no social security schemes or any other kind of government-sponsored elderly care, you’re basically left with three to four choices at best. While option one is to plan and invest for your retirement right now, the alternatives range from compulsory work post the age of 60, depending on your daughter or son, and in extreme circumstances, even living on charity. While the obvious choice here is option one, we have to factor in a number of elements such as your present age, no of years to retire, present income, expenses, and more.

Other variable factors may include family members who are dependent on your income as well as your risk-taking ability with regards to investments. Further complications include life expectancy on the rise due to advancements in medicine, as well as technology, healthcare services, and expenses taking a similar curve. This means that if the plan is to be completely self-reliant, not only do we need to account for a longer period post-retirement, we also need to account for inflation that could easily see expenses go up by 3-4 times exponentially during our retirement phase.

So how do people plan for a dignified and independent retirement while also factoring in the inconsistencies of life? Well, there are two methods followed globally, they are the replacement ratio method and the expense method.

Replacement Ratio Method

The replacement ratio method is quite simple and similar to how a government pension is calculated. For example, a person who is 45 years of age earning five lakhs a month right now, and set to retire in 15 years would earn 10 lakhs a month by the time he is 60. This is calculated keeping in mind a 5% increase in income year on year. Using this replacement ratio method, he can then choose between a replacement income of 50% (5 Lakhs), 75% (7.5 Lakhs), or 100% (10 Lakhs) for the rest of his life.

Expense Method

As the name suggests, the expense method is all about calculating expenses. As a more customized approach that’s tailor-made to each individual, the expense method helps plan for retirement by calculating all the expenses of the entire family while also factoring in future expenses taking inflation into consideration. For example, a person aged 40 with a monthly expenditure of about Rs.1 lakh, would have a monthly expenditure of about Rs. 2.25 lakh by the time he retires based on a 4% inflation, year on year. Similarly, expenses need to be calculated for every year that we’re retired, while accounting for inflation, all the way up to the age of 85, 90, or even 100. The tricky part, and this is where planning comes in, finding the present cost of investment to meet our forecasted future expenses.

As the saying goes, “the early bird gets the worm,” and this is no more evident than in our daily lives commuting to work. It’s when we’re late that we tend to make mistakes, break rules, jump traffic signals, or generally indulge in risky behavior. The same concept applies to retirement planning and it’s when we start investing early that we can afford to reach our targets by predetermined milestones, safely and without taking any risks. Think of your bank balance as correlating to your time left on this earth, if you have enough money left, you have enough time left, and you can even afford to stop and smell the roses.

In conclusion, the benefits of retirement planning are:

1.Dignity post-retirement.

2.Independence, freedom, self-reliance.

3.More options as to where you would like to retire (The Bahamas, Cabo Beach, Bali etc.)

4.The ability to be an asset to your family rather than a liability in your old age.

5.The ability to pay for expensive medical treatments or procedures without help.

6.Peace of mind not only for yourself, but for your spouse and children as well.

7.Last but not least, guaranteed quality of life post-retirement.

With rising inflation, reducing interest rates in our country, and the current situation in the world being the way it is, unless you plan to inherit a fortune or pull off a money heist, it’s time to start planning and investing. Like we mentioned earlier, the replacement ratio method is a great first stepping stone and gives you a good idea of where you’re at and where you need to be. Please remember, keeping a track of your expenses and being aware of how much you need to save is half the battle won, the rest as we already mentioned, is just discipline.

Hi readers, hope our previous article on wealth management and the various strategies associated to it was genesis to your financial discipline. This week, we would like to take you through the importance of nomination in any form of investment/saving choices you make.

As of 2018, the amount of unclaimed deposits in Indian banks and insurance corporations accounts to 34,000 crores INR. And the trend continues to grow north each year. The major factor that contributes to the accumulation of unclaimed money is failure of a nomination or the nominee being unaware of such deposits or investments made.

I am sure your hard earned money does not deserve to go unclaimed and a simple act of choosing to enter a name in the nomination column would ensure that your loved ones gets the benefit of your investments/savings in the event of an unfortunate departure.

What is Nomination?

Nomination in banking/financial terms refer to the process through which an account holder executes his right to appoint a person as the one who is entitled to receive the monetary benefits accrued out of an investment or saving venture in case of death of the investor or the account holder. And this simple and easy step would ensure the very purpose for which the savings/investment was started is served. It is an ideal way to lessen the hardships of the legal heirs in settlement of claims expeditiously in the event of the death of the account holder. A nomination can be typically done either at the time of opening of the account or at any subsequent time during the tenure of the account/investment. There are certain specific nominations forms that you need to complete and submit to the Bank/ Investment for completing the nomination.

Who is a Nominee?

A nominee is a person who is selected as the beneficiary for the savings/investments made by the investor or the account holder in the event of death of the account holder. However, you can have multiple blood related person as a nominee for your various accounts/investments.

Who can be a Nominee?

You can nominate any of the below-mentioned members of your family.

• Spouse

• Mother

• Father

• Son

• Daughter

• Brother

• Sister

Why is nomination critical?

Nomination enables your loved ones, access to your savings/investments in the occurrence of the eventuality without any hassles and delay at a time when they would be in most need of it.

Things to remember while nomination

Do mention the nominee’s name instead of addressing only their relationship with you (Mention the full name, age and address).

While nominating a minor as a nominee, appoint a person who is a major as a guardian giving his full name, age, address and relationship to the nominee.

What if you have failed to nominate already?

You do not have to worry if in case you have failed to do so. You still have the option to add nominations at any time during the tenure of your investment/savings. Please ensure that your nominee’s information are filled up accurately in the nomination form to avoid any later hindrances for the nominee. Also a nomination can be cancelled or changed by the account holder/investor anytime during his life.

Hope this article was helpful to you in understanding the importance of Nomination in any investment or saving endeavor. We will catch up again with another interesting topic that will help you to make progress in your financial goals. You can also let us know which topic you would want us to write in the comment box below.

Hi Readers,

Hope our previous article on the importance of Nomination was informative and useful for some of you. If you have not yet had the chance to read the same, you can find it here.

This week, we would like to share our thoughts on Gold – India’s evergreen love.

Gold – A metal that is most popular among the ornamental metals has never lost its glory. And the global pandemic is no exception. As a passionate investor, many of you might have already been into gold already. However, the following article will help you make an appropriate investment choice in gold that is tailored for you.

Why Gold is precious?

Being a derivate product of a natural resource, gold like oil resources is not abundant. The reasons people tend to make a gold investment are also diverse, as gold is simply ingrained in some cultures as a form of wealth and saving, whilst in other countries and for other individuals, it’s more about hedging financial market risks, as well as wanting to hedge against rising inflation.

Advantages of Investing on gold

Immune to inflation

Gold has historically been an excellent hedge against inflation, because gold has an immune system that withstands the tremors of a global economic crisis. Over the past 50 years global investors have seen gold prices soar.

High on demand - In spite of holding an uptrend in market price most of the times, the demand for this metal superstar has always been there no matter what. The most important reason is that Gold is held prestigious in many cultures of the world, especially in countries like India where almost no auspicious moments are complete without the presence of gold.

Liquidity - Another factor that makes your choice of investing in gold is its liquidity. In any investment, the ease with which you can buy and sell an asset plays an important role, and with over USD $100bn in daily commodity trade is one of the easiest of assets to buy and sell at any time.

Diversification - The key to diversification is finding investments that are not closely correlated to one another; gold has historically had a negative correlation to stocks and other financial instruments. Recent history bears this out:

• The 1970s was great for gold, but terrible for international stocks.

• The 1980s and 1990s were wonderful for stocks, but horrible for gold.

• 2008 saw stocks drop substantially as consumers migrated to gold.

Source: www.goldprice.org

Historical Gold Performance

In the year of 1974 the gold index was formed 1 ounce (28.35 grams) = 100 US dollars. If you see the above the chart from 1974 – 1981 the gold price moved from 100 USD to 850 USD which is a compounded annual return of 35.7% after which gold price hit a bottom of 350 USD in the year 1983. If you see the chart closely from 1983 – 2002 for about 19 years there was not much appreciation in gold price. In another analysis from 1981 – 2008 in fact gold was underperforming, there wasn’t any appreciation, having said that gold has delivered a positive return of 7% per annum since inception.

Why this international correction has not had a greater influence on the gold price in India?

In spite of the fluctuations in international gold price, it did not had any impact in India as the Indian currency (INR) has been depreciating consistently against the US dollar year on year that negated the depreciation of gold price and made gold prices to not fall down in accordance with international gold price in India. You can see the chart below for the years 1973 – 2020 how the US dollar has appreciated against Indian currency year on year.

1973 - 1 US Dollar = Rs. 7.63

2020 – 1 US Dollar = Rs. 73.77

Source: https://www.chartoasis.com/usd-inr-historical-data-download-cop0/

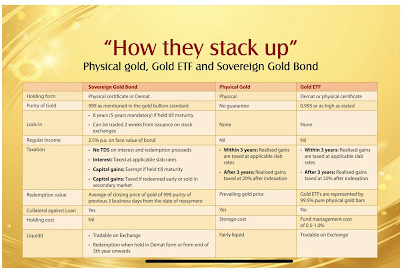

Types of Gold Investments

Physical Gold- Jewelry, Coins and Bars

Gold Exchange Traded Funds (ETF) and Exchange Traded Commodities

Gold Funds – Investment made in gold mining companies

Should you start investing in gold?

The answer is yes, you must allocate certain amount of funds periodically to invest in gold as an asset class. However, the percentage of investment in gold or any other asset for that matter varies from one individual to another. You need to customize your investment based on your overall income, expenditure, short term and long term goals.

So far, we saw the historical performance of gold, benefit of investing in gold and types of investment options available in gold as an investment. Our next articles we shall take a detailed look in to the Gold exchange traded funds and gold mutual funds.

You can also let us know which topic you would want us to write in the comment box below.

Greetings,

We hope you found our previous post on the Overview of gold investment and its historical performance both useful and informative. If you haven’t had a chance to read it yet, we’ve put it here so you don’t miss out!

Is your life insurance airtight?

Many consider insurance as the first step to building a savings portfolio, after all, there’s nothing as important as securing what you already have, beginning with the most important asset, your life. Life insurance salesmen are quick to ask the question “what would life be like for your dependents in the case of your untimely demise?” What most of them fail to tell you, however, is that if an unfortunate event does occur when you happen to be in debt, it’s your creditors who are going to benefit from your policy and not your wife or your children as you intended. That’s a pretty terrifying thought since the one thing that gives a person peace is a knowledge that the people who you care about will be looked after once you’re gone.

To elaborate, say a particular businessman passes away leaving behind about ten crores of debt ( outstanding loan) but also invested about 20 lakhs in life insurance for about 15 years which would mean his wife/or children would receive somewhere around 4-5 crores. In such a case the entire payout would go towards repaying the debt, along with any other assets he may have left behind, till the amount is recovered. This leaves us asking the question of whether there is no way for a man in debt to secure his family’s future or invest in life insurance without the proceeds being snapped up by creditors?

Well, of course, there is it’s called the Married Women’s Property Act or MWP Act and was originally set up in order to protect properties owned by women. Section 6 of this act covers life insurance policies and is the part that is most relevant today. According to this section, any married, divorces or widowed man can take a life insurance policy under this act which will cause said policy to automatically function as a trust under the Trust Act. While the trustees can be your doctor, chartered accountant, Advocate or financial advisor and the trustees can be changed at any time, the beneficiary ( wife& children ) can never be changed.

What does this mean, if you have any money invested in a life insurance policy under this act, in addition to it being safe from your creditors, even a court of law cannot attach it to any recovery of outstanding loan in case of your death. Furthermore, even in the case that you outlive the policy, the proceeds will still go to the beneficiary, making for a pretty airtight way to secure your wife and children’s future. A good rule of thumb before making such investments is to consult with a financial advisor or do some research on the human life value method or the capital need analysis method to figure out the ideal insurance cover for you.

If you enjoyed reading this post, please leave a comment or a suggestion on what financial topic you would like to read about next.

Greetings,

We hope you found our previous post on the Married Women’s Property Act useful and informative. If you haven’t had a chance to read it yet, we’ve put it here so you don’t miss out.

What a lot of people don’t realize while planning out their retirement is that interest rates for developing countries go down as they progress and develop. If you were sitting around thinking people in the US, UK, Sweden, Switzerland, or any other first-world country for that matter, were raking in big bucks on money sitting in the bank, think again. In fact, in some developed countries like Denmark and Japan, for example, they have negative interest rates and it actually costs you money to use the banks. Additionally, the US interest rate FED is just 0.25% at the moment, down by 1.25% from March this year.

What this means for pensioners or people planning their retirement is that in addition to accounting for inflation, they also need to account for lower returns on money sitting in fixed deposits or bank accounts. India for example, had private banks offering up to 8.25% for fixed deposits in 2015 while the current offerings stand at about 5.15% with an extra 0.50% for senior citizens. That’s a pretty sharp drop and means that if you were counting on interest rates remaining constant, you now have to recalculate and reconsider your retirement options.

A good way to counter the effect of declining interest rates on your retirement plan is by investing in schemes that offer a fixed interest rate over a longer time frame, this way whatever the current interest rate may be, your investment keeps earning at a predetermined rate. As we mentioned before, since rates go down as a country develops, this is a good thing. One such investment option for senior citizens, in particular, is the Pradhan Mantri Vaya Vandana Yojana (PMVVY) government-subsidized pension scheme.

While this scheme was initially announced a few years ago, it ended in March this year and was relaunched in May for a period of three financial years under new terms. In addition to a fixed interest rate over a period of ten years, this scheme also converts the interest into a pension that can be withdrawn monthly, quarterly, half-yearly, or annually. This is a great addition to your retirement portfolio as you can invest a maximum of fifteen lakhs per person which will provide you with a guaranteed monthly pension of Rs. 9,250/- for ten years. If you and your spouse invests fifteen lakhs each then you will receive a guaranteed monthly pension of Rs. 18,500/-

The cherry on the cake here is obviously the fact that in addition to ten years of fixed interest, you also get your principal amount back on maturation, making this a “win-win” situation. The rate of interest for policies purchased this current financial year will be 7.66%, while the interest rates for the remaining two years will be fixed as they commence. Life Insurance Corporation of India is the sole operator of this scheme which also includes a death benefit where as a beneficiary receives a refund of the purchase price in the event of your untimely demise.

In conclusion, with an unprecedented amount of uncertainty in the world today, having a constant source of income for a decade is an invaluable asset, albeit a small one. It’s many drops of water that form an ocean and every bit counts when you’re planning for your retirement. One downside may be the fact that you need to be at least 60 years of age and you have the option to surrender this pension plan under extreme circumstances like a medical emergency for you or your dependents. However, after completion of three years, you can avail of a loan against this policy up to 75% of the purchase price.

If you enjoyed reading this post, please leave a comment or a suggestion on what financial topic you would like to read about next.

Hi Readers,

Hope our previous article on the overview of gold investment and performance was informative and useful for some of you. If you have not yet had the chance to read the same, you can find it here. This week, we would like to throw light on the various investment options available for you in gold:

Physical Gold – An investment method that is most popular among Indians is direct purchase of gold in the form of jewelry, coins and bars, compared to the other forms of gold investments, investing in physical gold still remains a popular method to invest in gold. You can buy physical gold and sell it when you need the money. But when you buy gold as jewelry, there is a downside of making & wastage charges to it which may vary between 8% - 18%.

Digital gold – This is a new investment option that has been on the rise in recent time due to its easy access. You can purchase digital gold through the following apps:

Paytm, Phone pe, Google pay, and Amazon pay. For example: Paytm has tied up with Kalyan Jewelers for the delivery of physical gold or jewelry. Digital gold allows you to buy and sell gold at market price anywhere anytime. Each gram bought by an investor is backed by an actual physical gold in the vault by the vendor, which can be easily sold back online at market-linked gold rate.

Right now, there are three companies offering digital gold—Augmont Gold; MMTC-PAMP India Pvt. Ltd, a joint venture between state-run MMTC Ltd and Swiss firm MKS PAMP; and Digital Gold India Pvt. Ltd with its Safe Gold brand.

Downside: The price of the gold is higher than the MCX gold. It’s because there are three types of charges levied, convenience fee, trustee fees, storage fees additionally 3% GST and there is no regulator to look after this investment and the companies involved.

Gold Fund - Gold funds are a type of mutual funds that directly or indirectly invest in gold reserves. The money you invest in gold fund is used to invest in stocks of gold producing, distributing and gold mining companies. It is a simplest way to invest in gold without having to purchase it in its physical form. This investment reduces the risk of loss due to market fluctuations that accompanies the direct investment in gold. Gold mutual funds are ideal for investors who would like to diversify their portfolio and save them against the potential risk of loss from other investments. There are so many gold funds available right now in the market.

GOLD ETF - A Gold ETF is an exchange-traded fund (ETF) that aims to track the domestic physical gold price. They are passive investment instruments that are based on gold prices and invest in gold bullion. Gold ETFs are units representing physical gold which may be in paper or dematerialized form. One Gold ETF unit is equal to 1 gram of gold and is backed by physical gold of very high purity. Gold ETFs offer both the flexibility of stock market investment and the simplicity of gold investments.

Gold ETFs are listed and traded on the National Stock Exchange of India (NSE) and Bombay Stock Exchange Ltd (BSE) like a stock of any listed company. Gold ETFs are traded on the cash segment of BSE & NSE like any other company stock, can be bought and sold continuously at market prices.

In short, buying a Gold ETF would mean, purchasing gold in an electronic form. You can buy and sell gold ETFs just as you would trade in stocks. However, when you redeem Gold ETF, you don’t get the physical gold, but receive the cash equivalent of the quantity of gold. Trading of gold ETFs takes place through a dematerialized account (Demat) and a broker, which makes it an extremely convenient way of investing electronically in gold. Gold ETFs offers complete transparency of its holdings because of its direct gold pricing. Further, due to its unique structure and creation mechanism, the ETFs can lower your selling expenses as compared to physical gold investments.

Source: https://www.amfiindia.com/

Gold Sovereign bond - Sovereign gold bonds are RBI mandated certificates issued against grams of gold, allowing individuals to invest in gold without the burden of protecting the same. To know more about sovereign gold bonds, please read our earlier article on the same here.

Hope this article was helpful to you in understanding the investment opportunities in gold. We will catch up again with our insights on ‘Human Life Value and the science behind it’ which will help you to make progress in your financial goals. You can also let us know the topic that you want us to write about in the comment box below.

While most of the world is witnessing an economic slowdown of unprecedented proportions, India’s life insurance companies witnessed an 11.36% growth in their collective income during the fiscal end of March 2020. This has also been accompanied by a deluge of different life insurance products that can sometimes make it difficult for customers to navigate through the maze of policies and covers. Additionally, the absence of a standardized product can lead to miss-selling, as well as insurers contesting claims on various grounds.

We saw this happen in the health insurance sector during the pandemic, where a number of insurers were rejecting claims on grounds of misrepresentation or non-disclosure. While a standardized product called Arogya Sanjeevani was soon launched for the health sector, the life insurance sector was still lacking a standardized product. However, come January 2021, all Indian life insurance companies are mandated to provide a standardized life insurance policy called Saral Jeevan Bima, prefixed with the name of the Indian insurance provider.

In a statement released by the IRDAI, officials were quoted stating “customers often cannot devote adequate time or energy to make informed choices,” and “products may not be available for the intended sum assured.” This is why the new Saral Jeevan Bima is set to have “simple” features as well as standard terms and conditions. The policy can be availed of by anyone between the age of 18-65 with a maximum age of 70. Minimum and maximum terms are 5 and 40 years respectively, while the life insurance cover is between Rs. 5-25 lakh.

With the new guidelines in place, anyone who avails of this policy will receive ten times the annualized premium in case of the death of the policyholder, as well as the assured amount and 105% of all premiums paid as of the date of death. Additionally, single premium policy holders will receive 125% of all single premiums in addition to the assured amount. Last but not least, this policy will have no exclusions except a suicide clause. In conclusion, it’s about time the life insurance sector received some standardization, and such measures only serve to benefit consumers.

Greetings,

We hope you found our previous post on the Pradhan Mantri Vaya Vandana Yojana both useful and informative. If you haven’t had a chance to read it yet, we’ve put it here so you don’t miss out.

While the Mesopotamian shekel, the oldest known form of currency, was first used to trade over 5,000 years ago, it wasn’t till the 1920s that Dr. Solomon S Huebner managed to calculate what a person’s life is worth. Yes, the process of buying and selling human beings probably predates our earliest historical records, but what we’re talking about here is human life value in the context of insurance coverage. Human Life Value or HLV is an economic theory to put a monetary value on a human’s life in order to select appropriate life coverage.

This is quite simply the process of calculating the total economic loss caused to a person’s next of kin, which comes in addition to the obvious mental and emotional trauma that comes with a death in the family. While you can’t put a price tag on the latter and only time can heal such wounds, it’s the economic loss that we are interested in putting a price tag on. It may sound disconcerting at first to have to assign a monetary value to a person’s life, but the reality is that without such preparedness, grief would undoubtedly be accompanied by financial troubles as well.

This is probably why Dr. Solomon S Huebner talked extensively about developing a sense of responsibility among the general public and in particular, doing away with the myth that a person’s responsibility to his family is limited to his time in this world. Additionally, Dr. Huebner looked at any such shirking of responsibilities as a “crime of not insuring,” and even encouraged a “finger of scorn” to be pointed at anyone who was not interested in securing the future for their dependents.

Humans are social beings who depend on each other for strength and support. When you talk about Human Life Value, it’s basically the current, future, and potential financial support that you create for those who depend on you. This is done by taking into account a number of factors like your present age, what age you plan to retire at, annual income, employment benefits, and more. When you calculate all the variables and finally boil it down to one number, what you get is the final amount required to ensure that your death won’t affect the people you love financially.

Image Source : https://www.slideshare.net

Now ideally, you don’t want your dependents to have to depend on your life insurance coverage, but rather on the interest which is generated from the deposit of the insured amount. So while a simple way to calculate Human Life Value is obviously to calculate your monthly income from today till the time you retire, we’re going to look at four different levels of life insurance coverage.

1.Minimum level: The minimum level is where you cover yourself for up to 100 times of your monthly net income. For example, a man with a monthly income of Rs. 100,000 insures himself for 1 crore, which is 100 times his monthly income. This means his dependent can put this in a savings account at a 6% interest rate to earn Rs. 50,000 a month, which is 50% of his monthly income.

2.Adjustable level: In the Adjustable level you cover yourself for 150 times your monthly net income so the same 6% return on deposit would generate 75% of your monthly income.

3.Comfort level: The comfort level is where you get covered for 200 times of your net monthly income so, in case of any eventuality, your spouse will get the same amount as you were contributing to the family.

4.Considering future inflation: It is always wise to take into account future inflation and in such a situation it is recommended to cover yourself for 300 times of your monthly income so that your family receives 150% of your monthly income in the event of an unfortunate circumstance.

The interest rate, inflation and coverage differ from person to person & country to country. To find out the exact values kindly contact us.

In conclusion, death is hard to talk about, a lot harder to deal with, and most importantly, filled with uncertainty as no one knows when they’re going to die. That being said, the knowledge that you do know exactly how much your life is worth to your family and that you can prepare to have those needs met accordingly, is both comforting and reassuring.

If you enjoyed reading this post, please leave a comment or a suggestion on what financial topic you would like to read about next.

2. Vehicle Scrapping Policy. Vehicle Fitness Test after 20 years in case of Personal vehicle and 15 years in case of commercial vehicles

3. 64,180 crores allocated for New Health Schemes

4. 35,000 crores allocated for Covid Vaccine

5. 7 Mega Textile Investment parks will be launched in 3 years

6. 5.54 lakh crore provided for Capital Expenditure

7. 1.18 lakh crore for Ministry of Roads

8. 1.10 lakh crore allocated to Railways

9. Proposal to amend Insurance Act. Proposal to increase FDI from 49% to 74 %.

10. Deposit Insurance cover (DICGC Act 1961 to be amended). Easy and time bound access of deposits to help depositors of stress banks.

11. Proposal to revive definition of ‘Small Companies’ under Companies Act 2013. Capital less than 2 Cr. and Turnover Less than 20 Cr.

12. Disinvestment: IPO of LIC, Announced Disinvestment of Companies will be completed in FY 2021-22

2. Reduction in time for IT Proceedings: Reopening of Assessments period reduced from 6 years to 3 years except in cases of serious tax evasion cases

3. Proposal to constitute ‘Dispute Resolution Committee’. (Taxable income 50 lakhs and disputed income 10 lakh).

4. National Faceless Income Tax Appellate Tribunal Centre

5. Relaxations to NRI: Propose to notify rules for removing hardship for double taxation.

6. Tax Audit Limit: Proposal of tax audit increased from 5 Cr. to 10 cr. (Only for 95% digitized payments business)

7. Propose to provide relief on advance tax liability on dividend income.

8. Propose to include tax holidays for Aircraft leasing companies

9. Prefiling of returns (Salary, Tax payments, TDS etc.) Details of Capital gains from listed Securities, dividend income, etc. will be prefilled

10. Small Charitable Trusts. Increased from 1 crore to 5 crores (Compliance limit)

11. Late deposit of employee’s contribution by employer will not be allowed as deduction

12. Incentive to startup: Tax holiday exemption for one more year

13. Duties reduced on various textile, chemicals and other products

14. Gold and Silver (BCD reduced)

15. Agriculture Products: Custom duty increased on cottons, silks, alcohol etc.

What a lot of people don’t realize, is that there’s a lot more to mutual funds than the fact that they’re subject to market risk, and offer documents should be read carefully before investing.

While people who have a lot of money to invest can afford professional “money-managers” and diversified portfolios, mutual funds give the common man access to such professional money managing services. Think of it as a common fund or pool of money, where the public contributes and the collective amount is then invested by experts, according to the investment objective of the fund.

The different types of mutual funds are:

Equity funds - funds that invest in stocks

Debt funds - funds that invest in fixed income instruments

Money market funds - funds that invest in short-term money market instruments

Hybrid funds - funds that divide investments between equity and debt to create a balanced or diversified portfolio.

In this post, we’re going to take a closer look at Equity funds, in particular, as well as some variations of them. Equity Funds invest in stocks of companies and may further be classified in terms of the market capitalization of the target investment objectives.

These are:

Large-cap funds: These are open-ended equity funds that invest at least 80% of their assets in large-cap (1-100)stocks meaning big, established companies with excellent track record. These stocks are dependable and risk is comparatively less than mid-cap and small-cap.

Mid-cap funds: These are open-ended equity funds that invest around 65% of their assets in equity and equity-related instruments of mid-cap companies(101-250) or companies that are growing and progressing well but still no big enough to be classified as large-cap. The fact that many of these companies may soon progress to large-cap makes this segment quite lucrative for investors.

Small-cap funds: These are open-ended equity funds that invest around 65% of their assets in small-cap stocks(more than 251st) whic refers smaller companies. While these funds generally have an immense potential for growth, with a higher level of risk, of course. These funds are generally for investors with a high risk profile or to balance out a portfolio.

Microcap funds: These are open-ended equity funds which invest around 65% of there assets in publicly-traded companies that have a market capitalization less than small-cap companies. Like small-cap stock, micro-cap carries an even higher risk with explosive growth prospects.

All equity Funds can be classified into Active and Passive, where the fund is run by a team of experts and a passive fund mirrors a popular market index like Sensex, BSE.

The main advantage of investing in a mutual fund is that each investor, no matter how small the investment, gets access to professional money management service. Additionally, it would be quite difficult for an individual investor to build a portfolio that’s as diversified and spread out as a mutual fund on their own.

People often associate risk with luck, and while that may be true to an extent, the major difference is that unlike luck, risk can be measured. Now before we get into the ratios that help us measure how much risk is attached to a particular mutual fund, an important concept to understand is volatility. Volatility is basically the measurement of how erratic a particular fund is, so if a particular fund is highly volatile, what this means is it has a tendency to either rise or fall sharply in a relatively short period of time. This is why volatile funds are generally considered high risk.

Alpha

With an Alpha ratio, instead of comparing a fund's performance to its own average like some other ratios, we’re comparing its risk-adjusted return with a benchmark (example Sensex, Nifty). This is why an alpha ratio can be either negative or positive, with a negative ratio indicating a fund that is underperforming in comparison with its benchmark. For example, an alpha ratio of +3 indicates a fund that outperformed its benchmark by 3%, while -3 would indicate a shortfall of 3%.

Beta

Also called the beta coefficient, this one is a little different than the others since the value is going to be a fraction above 1 or a fraction below 1. What it is, is a measurement of the fund’s tendency to shadow the market as a whole, or to shadow a particular benchmark or index. So a value below one, like 0.7 for example, would indicate a fund that shadows the market up to 70%, so for every 1% change in the market, up or down, you can expect a 0.7% change in the fund. Similarly, a value above one, like 1.3, would indicate a fund that’s 30% more volatile.

Standard Deviation

This one is quite simply what we just explained with the definition of volatility, and is the measurement of how volatile a particular fund is, in relation to its own average. To elaborate, if a particular fund has an average return of 20% but also has a standard deviation of 10%, this means it could go 10% to 30%, or down 10%.

R-Squared

Since the Beta can be calculated against the market as a whole or any other benchmark, this can be misleading if the benchmark in question isn’t appropriate. This is why we have the R-Squared ratio which indicates the “relationship-level” between the fund and the index that’s being used to measure the Beta. R-Squared ratios go from 0-100, and while a 70 - 100 indicates an appropriate benchmark is being used and the Beta ratio can be trusted, anything below implies the Beta ratio is not a useful indicator.

Sharpe’s Ratio

Last, but definitely not least on our list, is the ratio developed by renowned economist and Nobel laureate William Sharpe, and is probably the most interesting of them all. Suppose a particular fund is performing really well and you are feeling really good about increasing your investment. What Sharpe’s ratio will tell you is whether the previous returns were due to smart choices by the fund manager or just higher risks being taken. This is why going by just one ratio can often be misleading as there are always a number of factors that need to be taken into consideration.

In conclusion, while everyone always talks about mutual funds being subject to market risk, no one tells you that market risk is tangible, can be measured, analyzed, balanced, and most importantly, accounted for.

When you think about mutual funds, the first thing that generally comes to mind is equity and the stock market. What a lot of people don’t realize, is that’s only half the story. For the more cautious investors, there are mutual funds that invest exclusively in fixed-income securities, that unlike equity, carry a lot less risk and deliver much better returns when compared with general banking products.

Mutual funds that invest in fixed-income securities are called debt funds and investments include corporate bonds, government securities, commercial paper (CP), certificates of deposit (CD), treasury bonds, and money-market instruments. Money-market instruments are funds that finance businesses for short periods of time in order to create a cash buffer to negate the gaps in payment cycles. These are great if you’re looking for a quick turnaround as investment options range from overnight to a year.

So the obvious question here would be “why doesn’t everyone invest in debt funds instead of putting their money in the bank?” The answer, debt instruments aren’t generally available for purchase because the minimum investment requirements put them out of reach of most retail investors. This is where mutual funds come in and make these fixed-security investments available to everyone who has a little cash to spare. Additionally, since these funds are all tied to some sort of corporate debt, they appreciate when interest rates fall.

Now there are about a dozen different types of debt funds and to keep it sweet and simple, we’re going to keep the definitions as short as possible.

First, we have them categorized by maturity period:

1. Liquid funds: Pretty self-explanatory, the main factors here are minimum investment period is 1 day, maximum period 91 days, and funds are invested in debt instruments that can be liquidated at any time. This is why liquid debt funds don’t have any lock-in period and redemption is typically processed in 24 business hours. Investments include different types of debt securities like treasury bills, certificates of deposit, commercial paper, and more.

2. Ultra-short-term funds: These have a slightly longer “wait-time” than liquid funds, come with a maturity period of anywhere from 3 to 6 months, and investments are exclusively in money-market and debt securities.

3. Low duration funds: Investments are in money-market and debt instruments while the maturity period is 6 to 12 months.

4. Short duration funds: Investments are in corporate and government bonds while duration is 1 to 3 years.

5. Medium duration funds: Investments are in corporate and government bonds while duration is 3 to 4 years.

We also have them categorized by investment portfolio:

6. Money-market funds: Investments are predominantly in money-market instruments and maturity is up to 1 year.

7. Corporate bond funds: Investments are predominantly in corporate bonds with a high rating (AA+ and above) and maturity is up to 1 year.

8. Credit risk funds: Investments are predominantly in corporate bonds with a rating of AA and below, and maturity is up to 1 year.

9. Banking and PSU fund: 80% investment in banks, public sector undertakings, and public sector financial institutions, the maturity period is 1 to 10 years.

10. GILT Funds: 80% invested exclusively in government securities, maturity period 3 to 5 years.

11. Floating rate funds: Since rising interest rates in the economy adversely affect banking and PSU funds, floating-rate funds offer more agility by investing at least 80% in fixed-income securities with variable interest rates. This means while the maturity is up to 7 years, the interest typically gets adjusted every 30-90 days.

12. Fixed maturity funds: Investments in high-rated debt securities and corporate bonds, investment is only available during a new fund offer, and maturity is predetermined.

In conclusion, if you don’t want to risk the stock market to get better returns on your money, debt funds are the next best thing. Not only do they come with quick turnaround times, they also minimize risk by investing in fixed-income securities.

As we looked at the different types of debt securities in our previous post titled “Meet the Money Market,” in this post, we’re going to look exclusively at money market funds and how they are a great way to make some extra returns in under a year. As we mentioned earlier, money market funds invest in money market instruments, and since the investment period is only 1 year, the portfolio is strategically diversified in order to maximize returns over that 1 year period.

These funds are highly secured since investments are only made in money market instruments issued by organizations with strong credit ratings. Think of it like this, instead of putting your money in a fixed deposit for a year, your lending it to organizations that have an excellent credit history, hence the two main characteristics of money market funds, low-duration, and low-risk. These instruments include certificates of deposits, commercial papers, treasury bills, repurchase agreements, and more.

Now while returns are not guaranteed, based on the liquidity of investments as well as the track record of the issuing companies, these funds are virtually risk-free. Additionally, it’s impossible to put your money to work on a corporate level of this scale as a retail investor, especially because the minimum “buy-in” is quite high. Money market funds, on the other hand, have low to no minimum investment requirements and are typically open-ended meaning additional investments can be made at any time.

The big question here obviously is “how much does it all cost,” and the answer is that while fund houses typically charge a TER (total expense ratio) based on the NAV (net asset value), as of September last year, SEBI has capped that at 1.05%. NAV is the current value of all the securities held by the scheme, minus liabilities, and this means fund houses cannot charge investors a TER that’s more than 1.05% on the NAV. This not only ensures malpractices like misselling and churning are avoided, but it also makes money-market funds more transparent and affordable at the same time.

As opposed to NAV which as we already mentioned, is net asset value minus liabilities, AUM or assets under management, is the cumulative sum of all the investments made by a mutual fund.

Now while all these funds have a 1-year option that gives better returns than most banking products, there are also 3-year and 5-year options that have higher returns.

In conclusion, Money market mutual funds are designed and calibrated for low-risk, low-duration returns that have minimum investment requirements and are available to the general public. Contact us for more information on how you can put your money to work, financing organizations with impeccable credit, from the comfort of your home.

To carry on where we left off with our previous post about money market funds, we’re now going to talk about the one single drawback to debt instruments, as well as the remedy. As we all know, debt instruments like corporate bonds, for example, decrease in value as prevailing interest rates go up. This is because when interest rates go up, people would rather put their money in banks than invest in bond funds at lower interest rates, causing the bonds to decrease in value. The inverse is also true here which means if prevailing interest rates fall, corporate bonds that were issued before the fall, will increase in value.

Greetings,

We hope you found our previous post on open-ended, fixed maturity funds, both useful and informative. If you haven’t had a chance to read it yet, we’ve put it here so you don’t miss out!

While 2020 ushered in a global crisis on a scale that humanity had never seen before, 2021 continues to teach us hard lessons earned over decades of practicing unsustainable economics. Pollution, strip-mining, deforestation, over-fishing, and hunting animals to extinction are just a few examples of the effect our economies have on the environment. As the world tries to move forward from the mistakes of the past, one of the things we’re trying to focus on is sustainability, and not taking more from the environment than we can put back. This focus is being delivered right at the root of our financial ecosystem by changing the way responsible investors invest their money.

Measuring sustainability

Sustainability today is measured in terms of E, S, and G, which stands for environmental, social, and governance respectively. Organizations that wish to be ESG compliant need to adhere to a stringent set of standards and regulations. While the environment score is determined by carbon footprint and the impact an organization has on the environment, the social aspect pertains to gender equality, social diversity, racial diversity, as well as diversity based on sexual orientation.

The governance aspect, today, has a lot to do with the ESG data that an organization makes available to the public, the quality of that data, as well as its transparency in operations. This is because financial disclosure and transparency are key aspects of ethical governance and organizations that are in compliance automatically become a much safer choice for investors. Given a choice between full disclosure and ambiguous operations, most investors would choose the former.

Indian ESG Funds

While assets managed by ESG funds globally reached a total of $1.65 trillion as of the December quarter of 2020, assets managed by ESG funds in India reached about 45 billion INR and continue to grow steadily. This is undoubtedly due to the effect the global pandemic has had on people and businesses around the globe. ESG funds weren’t that common pre-pandemic, however, 2020 saw a number of large asset management companies launch ESG schemes in India like the ones listed below.

Aditya Birla Sun Life ESG Fund

1.Started in December 2020 and managed by Mr. Satyabrata Mohanty.

2.Management is active while investments are 60-80% in large cap and remaining in mid and small caps.

3.Portfolio is focused 40-50 ESG compliant companies.

4.The fund retains the right to invest 35% of the fund’s net assets in ESG compliant international securities.

Axis ESG Fund

1.Started in February 2020 and managed by Mr. Jinesh Gopani.

2.This fund is focused on 52 ESG compliant holdings, the top 5 of which include Bajaj Finance, Kotak Mahindra Bank, HDFC Bank, Avenue Supermarts, and Tata Consultancy Services.

3.Management is active and return are at 31.20% since the fund’s inception on December 23, 2020.

4.Investments are 80% in stocks that rate highly on ESG factors.

ICICI Prudential ESG Fund

1.Started on October 2020 and managed by Mr. Mrinal Singh.

2.This fund is focused on 30 ESG compliant holdings, the top 5 of which include HDFC Bank, Kotak Mahindra Bank, Housing Development Finance Corp, Infosys, and Reliance Industries Ltd.

3.Management is active and return are at 10.90% since the fund’s inception on December 23, 2020.

4.Investment are predominantly in companies with a high ESG score. Stock selection is based on internal research as well as the Nifty ESG universe. The fund also reserves the right to invest in international organizations that are ESG compliant.

SBI Magnum Equity ESG Fund

1.Originally named SBI Magnum Equity Fund, this fund was relaunched as SBI Magnum Equity ESG Fund in May 2018 and managed by Mr. Ruchit Mehta.

2.This fund is focused on 39 ESG compliant holdings, the top 5 of which include HDFC Bank, Infosys, Tata Consultancy Services, Reliance Industries Ltd, and ICICI Bank.

3.Management is active and returns are at 10.84% as of December 23, 2020.

4.Investments are 80% in ESG compliant equity, while the remaining 20% in other equities, debt, or money market instruments.

Kotak ESG Opportunities Fund

1.Launched on December 2020 and managed by Mr. Harsha Upadhyaya.

2.This fund is focused on 48 ESG compliant holdings including Infosys,Bharti Airtel, HDFC Bank, Tata Consultancy Services, Eicher Motors,Larsen and Tourbo, Axis Bank, Ultratech Cement, Cipla, and more.

3.Investment is 95% in ESG compliant Indian stocks, 57.84% of which is in large-cap stocks, while 17.95% is in mid-cap stocks, and 9.63% is in small-cap stocks.

In conclusion, the world has changed in terms of environmental awareness and social consciousness and as responsible citizens of the world it is our duty to follow suit. Please feel free to contact us for more information on investing in ESG funds.

Greetings,

We hope you found our previous post on ESG funds both useful and informative. If you haven’t had a chance to read it yet, we’ve put it here so you don’t miss out!

A steady cash flow is the most important aspect of any retirement plan, and a lot of people look to Mutual Funds to either create or supplement a regular income. While a number of schemes exist that provide monthly or quarterly dividends, these are completely dependant on profits and hence cannot be classified as guaranteed returns. This is where SWPs or systematic withdrawal plans step into the picture and provide investors with a tax-efficient way to maintain a guaranteed cash flow while also outperforming a fixed deposit.

Disciplined withdrawals

A lot of people talk about discipline while investing, but not many about discipline while withdrawal which is an equally important aspect of maintaining a steady cash flow post-retirement. An SWP helps maintain discipline during withdrawal by redeeming a fixed amount of mutual funds every month, irrespective of the state of the market. This effectively does two things, it protects you from selling lump sums when the market is down, as well as overinvesting when the market is on a high, both of which are counterproductive if your aim is to create or supplement a steady income.

Now unlike a fixed deposit where you only withdraw the interest and your corpus remains intact, with an SWP, you’re actually withdrawing both, a part of your capital, and the interest. So say for instance you invest one lakh rupees to buy 10,000 units of a fund (NAV 10) and want a 5,000 INR monthly withdrawal. What will happen here is every month, 5,000 INR worth of units, based on the “Rupee-cost-average,” will be sold every month to supplement your income, irrespective of the state of the market.

Tax efficiency

This benefits investors in a number of ways, as opposed to a lump sum withdrawal which is subject to a single NAV at any particular point in time, Rupee-cost-averaging gives investors the ability to withdraw their funds at an average NAV that is collected over a longer period of time. This not only supplements your cash flow with fixed monthly returns but also gives your investment a longer period of time to grow and consolidate. Additionally, as opposed to interest earned from a fixed deposit that is classified as income and taxable as such, in an SWP, only the growth or profit is taxable as income.

To further elaborate, If 10,000 units of a fund that you bought for one lakh rupees grown to a value of 1.1 lakh rupees INR, registering a 10% growth, only 10% of your monthly withdrawal is taxable as income. Using the above example where the goal was to create a 5,000 INR monthly cash flow, only 500 INR will be taxable as income. When compared with the interest earned on a fixed deposit that is completely taxable, SWPs make a pretty good argument as a tax-efficient way to create a steady cash flow. To know more about SWPs and which ones are best for your portfolio, age, and risk profile, feel free to contact us.

Greetings,

In case you missed our previous post on systematic withdrawal plans, we’ve linked it here so you don’t miss out!

Greek physician Herophilus (325-280 BC), the father of anatomy, credited with the first ever scientific human cadaveric dissection, and arguably the greatest anatomist of all time wrote: “when health is absent, wealth becomes useless.” Fast forward to the 20th century and Mahatma Gandhi (1869-1948) famously said: “it is health which is real wealth, and not pieces of gold and silver.” While the timelines involved here are drastically different, what rings true across the centuries is the comparison between health and wealth, and the realization that one is quite useless without the other.

While both the distinguished gentlemen mention above hit the nail on the head while asserting that the pursue of wealth at the cost of one’s health is a rather useless endeavour, in today’s world, both are equally important. The connections between financial, physical, and mental health are undeniable. While poor health and healthcare bills can have a seriously negative impact on one’s financial life, poor finances can leave you unable to tackle a medical emergency or unable to recover from the cost of a medical procedure.

So if we can all accept that both are equally important, the problem then lies in the fact that while most parents and teachers instiil in us all the good habits to stay healthy, it’s a very rare occurence where someone teaches us about wealth in the same way. Luckily enough, since most people already knows the habits to stay healthy like brushing their teeth in the morning, drinking a lot of water, and getting enough sunshine and exercise, we can have some fun drawing parallels between good health habits and good wealth habits.